Cost Savings and Cost Avoidance: Why You Should Know the Difference

By: Lianabel Oliver

Many companies require their employees to classify the financial benefits of capital investments or organizational initiatives as cost savings or cost avoidance measures. For many non-financial employees, this classification is a gray area that is not well understood. If you have project management responsibilities, or responsibility for approving major capital or program expenditures, it is important that you understand the difference between these two concepts and how the information is reported on the financial statements.

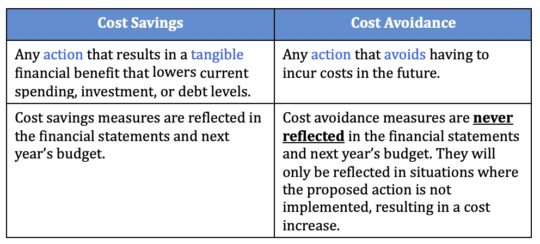

Cost-saving measures are any actions that lower current spending, investment, or debt levels. They result in a tangible financial benefit for the organization. The amount of money saved as a result of these measures should always be reflected in the financial statements and next year’s budget. Actual cost savings should be visible in the financial statements compared to prior periods; planned cost savings should be reflected in the budget. Some examples of cost saving measures are: reduction of overtime hours, elimination of temporary labor employees, negotiation of price decreases for products and services, or the negotiation of a lower rental fees for facilities and equipment.

Cost avoidance measures are any actions that avoid having to incur costs in the future. They represent potential increases in costs that are averted through specific preemptive actions. These measures will never be reflected in the budget or the financial statements. Some examples of cost avoidance measures are: a reduction of a proposed price increase from a vendor, the elimination of the need for additional headcount through process improvements, or a change in maintenance schedules for critical equipment to avoid work stoppages. The following table summarizes the major differences between cost savings and cost avoidance measures.

So, next time you justify a capital investment or organizational initiative to your management team, make sure you understand the difference between cost savings and cost avoidance. Accountants tend to review cost avoidance projects more closely because the financial benefits are not easily verifiable. You can only determine the impact of these measures if you do not implement the proposed action, in which case there will be an increase in costs. On the other hand, projects that are justified based on cost savings show tangible benefits, which are reflected in the financial results over time.

It is important that the management team establish a systematic mechanism to review all major capital investments and programs to ensure that expected financial benefits are obtained. Remember, if these are not achieved, it will probably result in higher product and service costs, which will lower your company’s profitability.